Wall Street is transitioning from a phase of defense to a phase of aggressive positioning, as the new Fed era, the return of liquidity, and new historic highs begin to reshape the structure of the markets.

In a previous article, we stated that we believed markets could enter a period of particularly strong bullish momentum starting from April 1st, 2026, as we considered that the majority of the geopolitical and energy shock had already been absorbed into valuations. The developments of the past few weeks confirmed this view, with global markets moving to new highs and the MSCI World Index even reaching new all-time highs, confirming that the market had already begun pricing in the next phase before it was fully reflected in the data.

The last fifteen days have been among the most critical periods for global markets in recent months. In an environment that only recently was characterized by geopolitical tension, energy shock, and fears of a new phase of instability, markets managed not only to absorb the risk but also to move once again toward historic highs.

The de-escalation of the crisis surrounding Iran, the gradual return of confidence, and the resilience of corporate earnings acted as the key catalysts behind this move. However, the most important element was not the rise itself, but the way in which it occurred. Despite the continued volatility in news flow and political statements, capital did not abandon risk. On the contrary, a clear restructuring of positioning took place, with flows gradually returning toward equity markets, technology, and sectors linked to the real economy.

This behavior confirms a historically recurring pattern. Markets usually complete the largest phase of fear before full visibility on developments even exists. In other words, the market does not wait for confirmation in order to move. It prices it ahead of time.

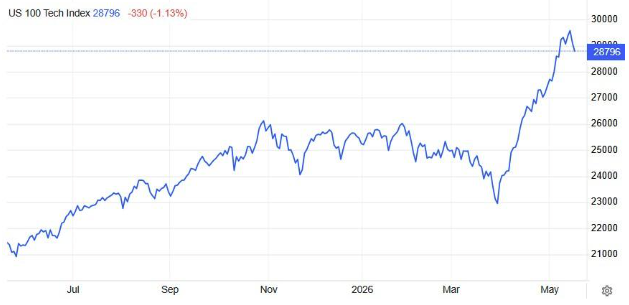

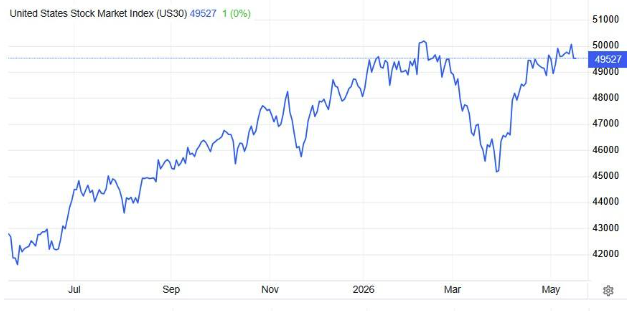

During this period, the major U.S. indices once again moved close to their highs, while technology continued to function as the market leader. Earnings announcements from the world’s largest companies confirmed that profitability and liquidity remain strong even in a higher interest-rate environment. This development is particularly important, as the U.S. market continues to be supported by corporate giants with combined market capitalizations of tens of trillions of dollars, which continue to generate growth and strong cash flows.

Another significant development for the markets is the expected SpaceX IPO in June, which is estimated to become one of the largest investment events of recent years. The focus of attention is not only on the company itself, but primarily on the size of the capital expected to be requested by investors, as this process may function as a barometer for risk appetite and liquidity conditions in global markets. Historically, IPOs of this magnitude occur during periods when the market begins regaining greater confidence in growth prospects and in the continuation of the bullish cycle, further reinforcing the view that Wall Street is gradually entering a new phase of expansion and more aggressive capital positioning.

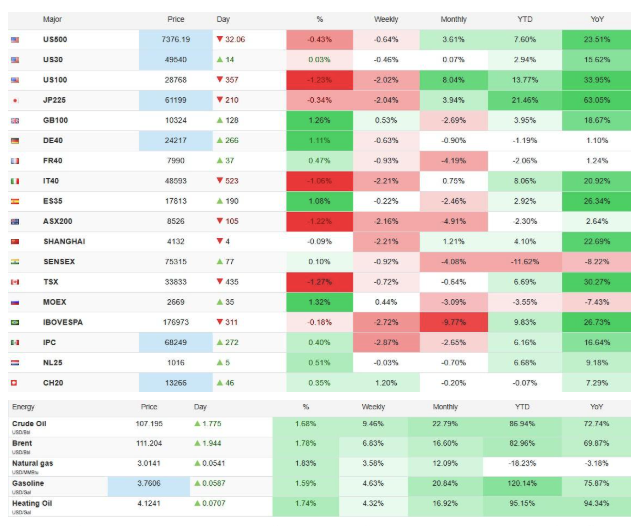

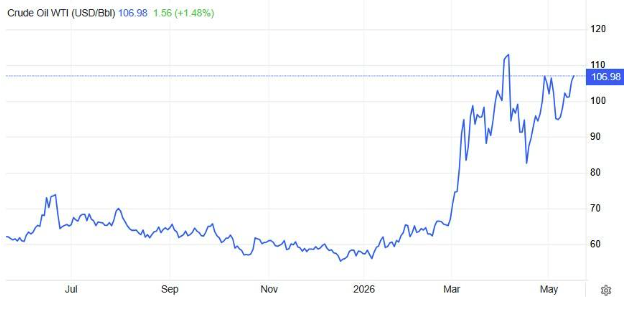

At the same time, particular importance should be placed on the fact that oil prices failed to move to new highs despite the intense geopolitical uncertainty that preceded them. This picture reinforces the view that the energy shock had more of a short-term reactionary character rather than marking the beginning of a new long-term explosive rise in energy prices. The gradual easing of energy costs is already acting as a supportive factor for markets, industry, and naturally for shipping as well.

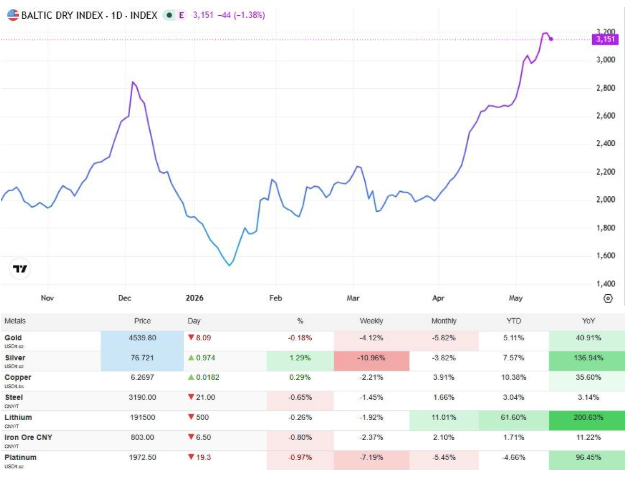

Shipping continues to present particular interest, as the Baltic Dry Index maintains strong momentum and confirms that demand for transportation and raw materials remains resilient. Our forecast for a move of the Baltic Dry Index above 3,000 points has also been confirmed, a development that further strengthens our view regarding the strength of shipping and global economic activity. At the same time, our strategic positioning regarding the particularly positive years we expected for shipping, already from the period when the Baltic Dry Index was near 900 points in 2025, also continues to be validated. This approach remained consistent despite many reports and estimates over the last 15 months, which focused primarily on recession scenarios and a significant slowdown in the global economy.

Importance should also be attached to the recent meeting between Donald Trump and Xi Jinping in China, as it represented one of the most significant developments of recent years in relations between the world’s two largest economies. It is worth noting that the last period of substantial rapprochement and high-level personal diplomacy between the United States and China had also taken place during Trump’s first term, between Trump and Xi Jinping, and not during the Biden-Xi period, a fact that gives even greater significance to current developments.

The discussions focused not only on trade and technology, but also on issues related to Iran, Taiwan, and geopolitical stability, confirming that both sides are seeking a new phase of management of global balances. At the same time, the scheduled visit of Vladimir Putin to China on the 20th of the month is also of particular importance, at a time when the global geopolitical chessboard appears to be entering a new phase of negotiations and repositioning of balances.

In our view, these developments concern not only U.S.–China or Russia–China relations but may also form part of a broader effort toward gradual de-escalation and a redefinition of international alignments, potentially even creating the conditions for future progress on the Ukrainian front as well. For the markets, every move toward stabilization of international relations and limitation of geopolitical tensions has historically functioned as a major positive catalyst for liquidity, investor sentiment, and risk assets.

However, the most important event of this period may not be earnings or geopolitical de-escalation. It is the beginning of the new Fed era.

The market is now beginning to price in a new phase of monetary policy following Jerome Powell. This transition carries far greater significance than a simple change of leadership. Historically, every major shift in Fed direction has affected not only interest rates, but the entire structure of markets, liquidity, and risk appetite.

In our view, the possibility of the Fed proceeding with interest-rate cuts in upcoming meetings can no longer be excluded, particularly if energy pressures continue to ease and geopolitical stabilization is maintained. The market is gradually beginning to price in an environment where the priority shifts from fighting inflation toward maintaining growth and liquidity.

And naturally, the enormous amount of capital that remains parked in money market funds should not be underestimated. In recent years, the Fed’s high-interest-rate policy drove historically high amounts of liquidity into low-risk short-term investment products, creating one of the largest “parking liquidity pools” seen in markets over recent decades (close to $8 trillion).

This has particular importance for the continuation of the cycle. In an environment where markets maintain bullish momentum, geopolitical conditions stabilize, and expectations for Fed rate cuts begin to strengthen, a development desired by President Trump, part of this liquidity may gradually begin returning to risk assets. Historically, such capital reallocations act as accelerators of bullish moves, as the market becomes fueled not only by improving psychology but also by real inflows of fresh liquidity.

In our view, the market is now entering an especially critical and potentially highly dynamic six-month period extending through the U.S. midterm elections. Historically, political cycles in America directly affect market behavior, particularly during periods when Wall Street functions as a key indicator of economic confidence for American voters.

Within this framework, we believe the Trump administration will seek to maintain as stable and positive an environment as possible, both geopolitically and economically. The de-escalation of international tensions, efforts toward agreements or ceasefires, support for growth, and the prospect of a more market-friendly monetary policy together create an environment that could become highly supportive of risk assets.

Wall Street has historically remained one of the most important “psychology indicators” for the American economy and for the political image of every administration. Historically, periods preceding major elections are often accompanied by efforts to preserve positive economic conditions, strong consumer confidence, and resilient markets.

In this environment, we do not believe the coming months will simply represent a phase of stabilization. We believe they could evolve into a phase of strong acceleration for the markets, as politics, liquidity, technology, and geopolitics begin aligning in the same direction.

History shows that the largest bullish phases do not begin when risk disappears. They begin when the market realizes that the worst-case scenario is probably not going to happen.

And in our view, the last fifteen days may have represented precisely this moment of transition.

In this environment, the question for investors is not simply whether markets can move higher. The question is whether we are already at the beginning of a new bullish cycle that most continue to underestimate.

The critical question for investors remains one:

Will you be part of this new liquidity cycle, or simply observers of it?

We believe that major investment opportunities are created during periods of transition, where uncertainty begins transforming into direction, and information into strategic positioning.

by Kotsiakis George