Private Wealth & Investment Strategist, Founder of Gekodesk & Partners

About a month ago, when we opened the analytical cycle for "The New Liquidity Cycle," we shared an assessment that went completely against the consensus of the media establishment: that as of April 1st, markets were much closer to the starting line of a powerful upward momentum rather than the beginning of a downward spiral. We insisted that the geopolitical and energy shock surrounding Iran had already been "digested" by valuations, and that smart money was looking at the day after long before it showed up in the data.

Today, in mid-June, the unfolding of events vindicates us completely.

As almost always happens, markets never waited for the official resolution of crises to react. They discounted it, absorbed the risk, and moved right back toward their all-time highs. And just like that, the total capitalization of the U.S. stock market officially hit the astronomical milestone of 65 trillion dollars.

But here lies the great illusion of the selloffs, and a phenomenon that most people fail to read correctly. Lately, the news cycle has been recycling terror, and the daily indices were showing losses, sparking a temporary panic. Yet, the total market capitalization refused to drop. Money wasn't evaporating; it was recycling internally.

The indices are making new highs even as the media blamed and criticized Trump's tactics at least 38 times, claiming that "the crisis in Iran was ending" due to flawed handling. The market bypassed them. When you consider that we started the year close to 55 trillion dollars, the current 65 trillion is not only far from being an "ideal ceiling," but in our view, it is still way too little for what we expect to unfold in the coming months.

This expansion of the pie is no longer just about a few Big Tech stocks. The American strategy is rapidly shifting toward tangible, physical reconstruction and supporting new trade agreements. Washington is closing deals, trading geopolitical stability for the procurement of massive infrastructure projects, creating an immense volume of business for the real economy.

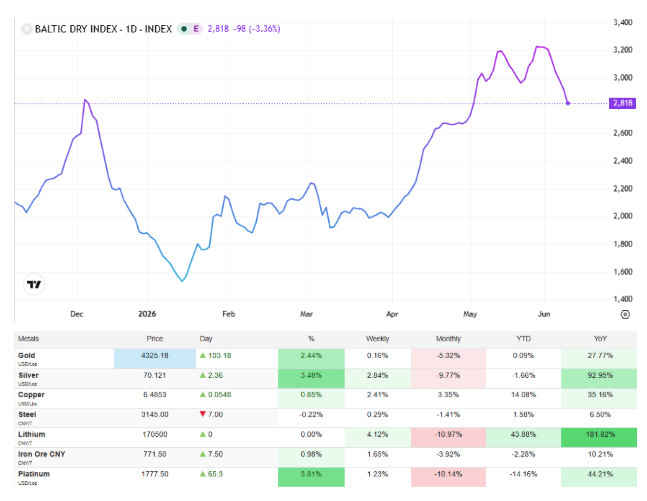

In this environment, shipping’s Baltic Dry Index (BDI), which we predicted would break through the 3,000 mark and is today undergoing a healthy correction at 2,700 - 2,800 units, offering an excellent buying opportunity, is not the only one sending signals. The big move is now happening in complementary indices: industrial metals, infrastructure, logistics, and the Dow Jones Transportation. That is where you find the supporting companies that are called upon to carry the weight of this massive demand.

The same thing is happening with the technological revolution, which over the next two years is moving from the software level to physical infrastructure. Congress just approved the bill for 70 billion dollars in government investments exclusively for the Trump administration's AI initiatives. Let's remember how fiercely analysts were criticizing the efficiency of AI investments over the past few months. Reality is leaving them behind. This 70 billion state funding will act as a multiplier because artificial intelligence needs physical things to function: Data Centers, power grids, and logistics lines.

At the same time, we are observing an exceptionally important statistic: the S&P 500 has not made the same percentage gain since the beginning of the year as the Nasdaq, which is galloping to new historic highs. This imbalance screams what we have always been writing: a major Sector Rotation is brewing. Capital is moving toward sectors of the real economy that promise high yields.

The ultimate confirmation of how strong risk appetite remains came from the historic public offering of SpaceX on Nasdaq, the largest IPO ever recorded. This serves as a triumphant personal vindication for Elon Musk, whom many in the past used to mock for his strategic alliance with Trump.

The big question is where this ocean of liquidity will head next. The answer will lock in on June 26th, with the completion of the reconstitution and the new evaluations of the Russell 2000 index. This year, FTSE Russell is introducing a semi-annual reconstitution split for the first time, accelerating the movement of capital.

In an environment where the Fed, under Kevin Warsh’s highly anticipated first official speech in the post-Powell era this Wednesday, is expected to permanently silence the media chatter about new rate hikes, the small and mid-cap companies of the Russell 2000, which are highly sensitive to borrowing costs, will become the ultimate capital magnet.

We do not believe there should be a rate cut right now, at this Wednesday's meeting. A rushed easing move would be perceived as a loss of the Fed's independence against political pressure, and the market would react negatively. However, our strategic outlook remains clear: the horizon leading up to the U.S. Midterm elections promises a series of substantial cuts, which will total up to 0.75 basis points.

This American strategy of realism stands in stark contrast to Europe’s leadership deficit. At the current G7 Summit (June 15th to June 17th), Europe arrives trapped in an agenda of new sanctions against Russia and tight monetary policy. Instead of the European leadership looking for ways to end these detrimental policies, it continues a tactic that, as we have been emphasizing for a year now, steadily increases the bill of losses for the European economy.

The price is vividly reflected in the automotive industry, a sector Europe dominated for decades. Within just a few months, Chinese manufacturers have taken a seat at the decision-making table both geopolitically and developmentally, doubling their market shares, especially with their automotive industry. Meanwhile, historic giants like the Volkswagen Group are forced to discuss factory closures in Germany, and component leaders like Bosch and Continental are moving forward with mass layoffs.

At the end of the day, the market possesses the most potent fuel available: 8 trillion dollars currently sitting on the sidelines in money market funds. The moment the new Fed flashes the final signal of stability, this ocean of massive liquidity will flow back into the risk assets chosen by the investment rotation, acting as a violent accelerator for the upward move.

In such a complex and fast-paced environment, the true value of an investment advisor becomes crystal clear. The media will always generate noise and artificial panic. The role of the professional advisor is to act as a shield, to help the investor not just protect themselves from the noise, but to calmly exploit it to their advantage, turning the fear of the masses into an investment opportunity for their own portfolio.

Already, many of the things we have been pointing out to you since the beginning of the year have become facts. It will be our great pleasure to summarize all of them, backed by evidence and numbers, in a major review article right after the end of the first half of the year.

Until then, the critical question remains one:

Will you be part of the new liquidity cycle, or mere observers of it?

by Kotsiakis George