As we approach the closing of the first half of the year, the global investment community is faced with a familiar, recyclable noise. The Federal Reserve's recent "hawkish" verbal interventions and predictions by certain analysts of potential new interest rate hikes are merely communication-driven expectation management, essentially jawboning, aimed at keeping the market on edge and artificially suppressing sentiment. Our assessment at Gekodesk & Partners remains steady and clear: interest rate hikes have completed their cycle. The political schedule in Washington is pressing relentlessly, and the path toward the crucial midterm elections renders interest rate cuts a one-way street in the coming months, to ensure the necessary economic stability and growth momentum. Central bankers know all too well that they cannot risk a credit event in an election year, and liquidity will return to the system one way or another.

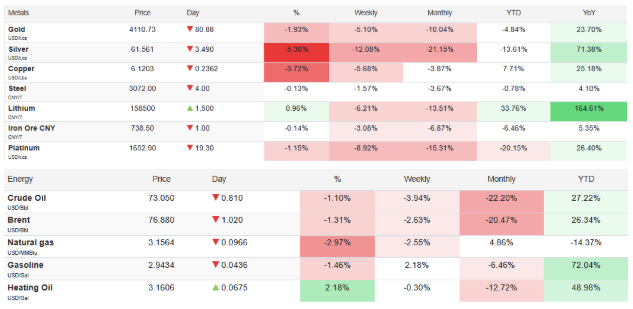

At the same time, geopolitical nervousness surrounding Iran is systematically being used by major institutional players, Market Makers, and the mass media as a fear-mongering smokescreen, allowing strong hands to sweep up liquidity and quietly build massive positions at lower valuations. The fundamental data of the real economy refutes these terror scenarios daily. The Straits of Hormuz remain open, shipping moves uninterrupted, and the prices of marine fuels, as well as oil, have already corrected significantly, returning close to the levels seen before the onset of the crisis. While we expect even lower price levels for the black gold market as global supply stabilizes, the picture in the freight market is entirely different and represents the true tip of the spear. We anticipate a powerful, autonomous movement in freight rates, with the Baltic Dry Index soon breaking upward through the 3,000+ point milestone once again, confirming that global trade turnover maintains its underlying, unshakeable momentum.

The real event that captured the structural shift of our times and was etched into global economic history in recent days was the emergence of the planet's first official trillionaire. This milestone completely changes the rules of the game, shifts the technical balances, and elevates Wall Street's psychological ceiling. The alleged concerns propagated by the media regarding the valuations and future returns of tech giants, the so-called Big Tech, constitute the perfect alibi to trap retail investors and force them out of the market. Achieving trillionaire status has now become the new grand target and the ultimate benchmark that other technology and artificial intelligence leaders will seek to conquer in the months ahead, triggering a new cycle of inflows and re-rating.

Besides, numbers never lie for anyone who knows how to read them behind the bombastic headlines of the news. While the consensus panics over inflationary pressures, reality shows that the spike was purely energy-driven and is already deflating along with oil prices. At the same time, the true driving force of Wall Street is the monstrous leap of over 10% in business investments in technology and AI infrastructure. The American economy is not on a path toward stagflation, but rather in a phase of controlled "Goldilocks" growth, where second-quarter corporate earnings will come to validate the structural strength of Big Tech, providing the necessary fuel for the next breakout of the indices.

The validation of this strategic move is hidden within the current behavior of the ticker itself, which short-term players fail to interpret. While May closed strong, June has evolved into a period of intense accumulation, with the main US indices recording returns that flirt with zero or move into slightly negative territory. This flat image is not a sign of fatigue, but the ideal smokescreen. During these weeks of apparent stagnation, large institutional managers are building new, powerful positions across a range of undervalued sectors with surgical precision. This quiet reallocation of capital and the "scooping up" of shares constitute the necessary preparation for the next big move, in our opinion. When the second-quarter corporate earnings announcements begin to hit the public eye in less than a month, strong fundamentals and valuations will act as the ultimate, violent fuel. The accumulated energy of this "shallow" June will be unleashed, turning today's uncertainty into the catalyst for the continuation of the great upward rally.

All these critical market signals translate into real alpha and surplus value for the investor only when their investment advisor is capable of timely reading their existence and pointing out the correct way to exploit them. This reality is perfectly proven by our steady track record. For a long time now, we have been consistently informing you about the strong positive momentum of the markets, which continued to chart new historical highs, even amidst the greatest geopolitical and energy crisis of recent decades. This is precisely the role of a true strategic advisor. Through our regular column in Maritime Economies, you always secure the most timely, penetrating, and valid briefing on the upcoming trends of the global economy. As the indices gather strength and we count down the days, the big question on the table is now clearly semiotic and political: will the Trump administration, in the historic celebration of Independence Day marking the 250th anniversary of the United States, manage to lead Wall Street to an absolute, celebratory close at new historical highs? Gekodesk & Partners remains on the ramparts, waiting for the Bull Scenario to deliver its final answer on board.

by Kotsiakis George