As we enter the opening days of July 2026, the landscape across global markets is shifting dramatically, reinforcing the critical importance of a rigorous portfolio diversification strategy. The first half of 2026 was defined by stark divergence between markets, confirming that the phase of universal, broad-based gains has gradually given way to an environment of heightened selectivity. Developments over the past month have largely validated our baseline scenario. We had anticipated a dual-pronged movement leading up to the July 4th milestone: on one hand, that the U.S. market still possessed the liquidity and structural fundamentals to push toward new historic highs, and on the other, that oil prices would see a significant reduction in risk premium, falling below the levels seen before the onset of geopolitical conflicts in the region of Iran. Seasonality and the internal dynamics of capital flows provided strong support on Wall Street, enabling the Dow Jones to break through the psychological and historic barrier of 53,000 points, as institutional portfolios sought to lock in returns ahead of the summer season, precisely as energy costs began to ease noticeably.

This dual closing marked the culmination of a first half filled with intense volatility and massive divergence across equities, commodities, and energy. The S&P 500 completed the first half of the year with a robust advance close to plus 10%, while the Nasdaq, driven by Artificial Intelligence, recorded gains of 18%. Notably, the U.S. market demonstrated remarkable resilience, managing to sustain a stabilizing momentum throughout June following an exceptionally positive and profitable May. This ongoing ascent was even more clearly reflected in the S&P 500 Equal-Weight Index, which moved higher to plus 12%. This performance proves that the rally has ceased to be top-heavy and has begun to spread healthily across the entire spectrum of the U.S. market, well beyond the familiar tech mega-caps. Within this broad May-June foundation, our research has identified several hundred companies that have lagged and whose valuations remain exceptionally depressed, creating an ideal environment for selecting quality equities with a low risk profile.

The real surprise of the half, however, was written in the North Asian markets, where returns reshaped the balances within global portfolios. Due to their central positioning in the global supply chain for semiconductors, chips, and next-generation advanced memory units, Asian indices recorded a vertical ascent. South Korea’s KOSPI index emerged as the absolute outperformer globally in the first half, registering a legendary rally of plus 170% year-to-date (YTD), propelled by the explosive outperformance of tech hardware and next-generation semiconductor companies. Concurrently, Japan’s Nikkei delivered one of the finest first-half performances in its modern history, closing the first half of 2026 with impressive gains of plus 38% YTD. In Japan's case, a catalytic role was played by the ongoing, historic depreciation of the yen, which functioned as a double engine for growth: on one hand, it hyper-charged the profitability of the country’s major export giants, and on the other, it rendered Japanese asset valuations exceptionally attractive to foreign institutional capital investing with strong currencies. This geographical shift in investment intensity demonstrates that the tech infrastructure trade is no longer just about software but is handsomely rewarding the economies that produce the hardware of the new digital era.

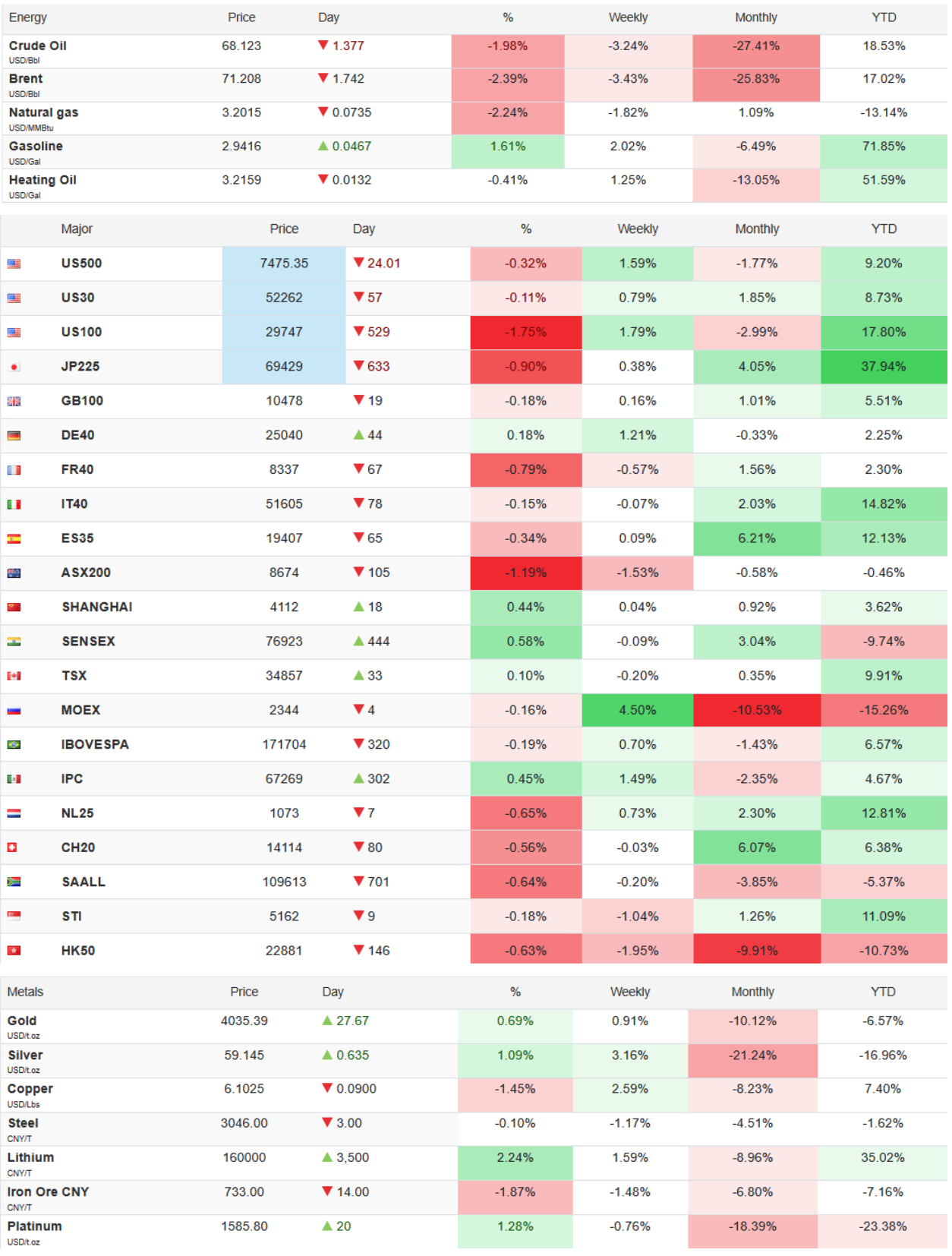

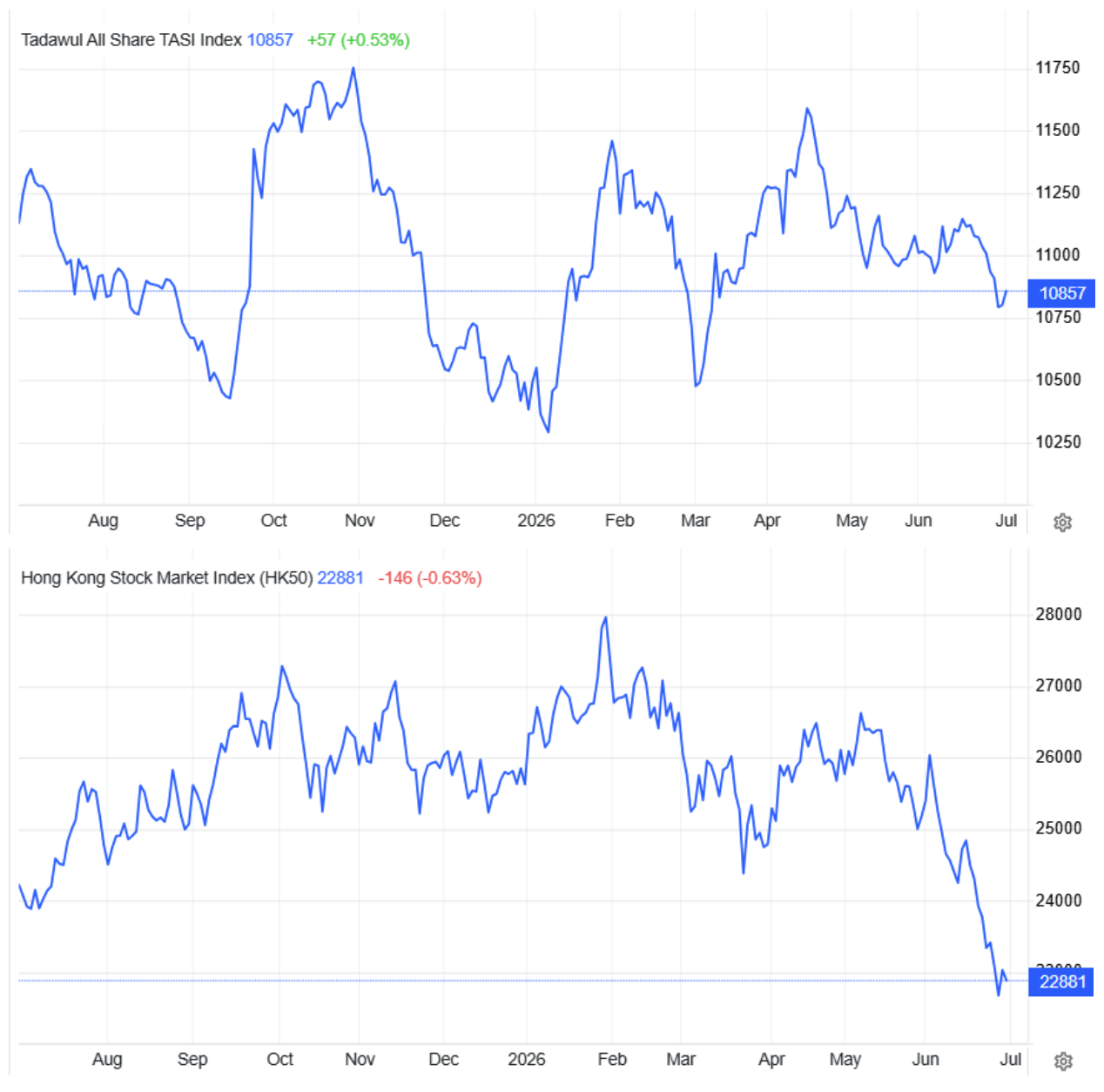

In stark contrast to this Asian euphoria, China stood out as the great exception and the most resounding disappointment of the first half, moving in an entirely opposite trajectory from its neighbors and confirming the deep structural crisis it is undergoing. The divergence of the Chinese market from the rest of the world is truly chaotic. The Hang Seng Index in Hong Kong concluded the half with significant losses of minus 11.5% year-to-date, with the sell-off accelerating dramatically during June, where it shed 9.1% of its value in just a matter of weeks. A similar picture was painted by the major Chinese ETF, the iShares China Large-Cap (FXI), which tracks the fifty largest companies in the country, recording a violent drop in the range of minus 12% to minus 13% since the beginning of the year. This capital flight from Beijing was fueled by the fact that the domestic real estate market remains completely frozen, keeping consumer confidence at historical lows, while raising fears over the incoming Trump 2.0 administration and threats of universal tariffs have spooked Western institutional investors. Furthermore, due to strict U.S. sanctions, China has been sidelined from the cutting edge of the global tech rally, unable to benefit from the Artificial Intelligence boom. However, within this setting of severe pressure on China, we believe that some of the most high-quality and high-yielding investment opportunities globally are currently hiding. Valuations of premier Chinese giants with massive liquidity and remarkably healthy cash flows have been compressed to such extreme levels that the risk/reward ratio is becoming exceptionally attractive for patient portfolios looking to buy value in periods of generalized fear.

In the commodities and energy markets, the first half was similarly marked by major reversals, with crude oil acting as the absolute mirror of geopolitical risk. During the preceding months, crude oil prices had staged a violent rally, fueled by the prolonged blockade at the Strait of Hormuz, which directly threatened global energy flows. However, the past week brought a historic turnaround. The White House announcement regarding the signing of a memorandum between the United States and Iran fundamentally altered the sentiment in international markets, clearing the way for the full reopening of the Strait and the relief of the supply chain. The price reaction was immediate. Brent completed the half falling steadily toward 73.12 dollars a barrel, a level below the valuations that stood prior to the military escalation in the region, confirming the gradual removal of the geopolitical premium and providing a massive breather for central banks battling inflation.

This trend in energy worked in tandem with another highly critical development for global trade and shipping. The Baltic Dry Index (BDI), which reflects the trajectory of the dry bulk shipping market, recorded an impressive surge of a cumulative plus 77% year-to-date. This explosive path of the BDI proves that global demand for physical raw materials, industrial metals, and global logistics remains exceptionally robust. In the currency markets, the U.S. dollar managed an impressive comeback, reversing the downward trend with which it began the year. The DXY dollar index rebounded dynamically from its lows of 95.5 and closed the half above 101, booking a gain of roughly 3% since the start of the year, as Kevin Warsh’s stern stance made it clear that U.S. interest rates will remain elevated for a longer period.

This abrupt comedown in energy costs arrives at a pivotal juncture, as the Federal Reserve attempts to balance on an exceptionally thin tightrope. May data showed that inflation ran at an annual pace of 4.1%, marking the highest level since the spring of 2023, with the core component at 3.4%. In his first official appearance, the new Fed Chairman, Kevin Warsh, demonstrated absolute resolve, maintaining interest rates in the 3.5% to 3.75% range and making it clear that the 2% target remains completely non-negotiable. Nevertheless, the bond market is already treating these inflationary figures as backward-looking data, precisely because they have not had the time to price in the recent collapse in oil prices. The retreat in U.S. 10-year Treasury yields toward 4.41% confirms that major institutional players see a gradual normalization ahead rather than a new flare-up in inflation.

As we step into the second half of 2026, the strategy of Gekodesk & Partners focuses on decoding these newly formed balances. Our tracking is centered on how the drop in energy will translate into corporate profit margins ahead of the Q2 earnings season starting from July 14th. Sectors such as transportation and airlines, which face severe pressure, are expected to show improvement. Concurrently, the market will have to adapt to the Fed's new management style, which under Warsh lacks traditional forward guidance and decides on a meeting-by-meeting basis based on real-time data, meaning greater short-term volatility.

In this context, within July we will publish in the pages of Maritime Economies magazine our comprehensive, detailed, and retrospective feature reviewing our articles for the entire first half of the year. This special edition will include, in their original form, all that we recorded and analyzed during the previous months, capturing exactly how our strategic assessments and core scenarios materialized into action across international markets. This move stems from our firm belief that an investment advisor and wealth manager is not judged by generic, post-mortem commentary, but by the ability to read macro developments and market trends far ahead of the broader public. This track record serves as the absolute compass for your next moves.

The core conclusion is simple. The market is changing its skin. The era of blindly allocating into indices is officially over. The remainder of the year belongs strictly to rigorous stock-picking and a deep understanding of macroeconomic rotations, positioned calmly where valuations have become disconnected from the true intrinsic value of businesses.

by Kotsiakis George